Investment Fundamentals Explained

With the launch of New NISA (Japan’s revised tax-free investment program), people who have never invested before are entering the market in growing numbers.

This article is written for both those already investing and those who want to try but feel nervous — I hope it helps you grasp at least the basics of the investment world. (This reflects the latest situation as of January 2024, when this article was written.)

The focus is on the big picture: overall trends, their meaning, and how to think about them. I’ve kept the technical detail low, so beginners can read comfortably.

I’ll also touch on investment targets you may be curious about — stocks, bitcoin and other cryptocurrencies, investment trusts — as well as the New NISA system.

Should You Even Invest?

If you’re reading this, you’re clearly interested in investing. But many beginners wonder: “Is investing really a good idea? Isn’t it dangerous?”

Let me start with the conclusion: there is no such thing as an absolutely safe investment. However, if you have the right knowledge in advance, managing risk appropriately is not that difficult.

In general, low risk means low returns (low-risk, low-return), while high risk comes with the potential for high returns (high-risk, high-return).

Many products claim “low risk, high returns!” or guarantee principal, but over 90% of those are scams. The existence of such scams has led many people to believe “investing is dangerous!” — as have those who experienced the trauma of a bubble collapse.

Certainly, scam products are real, and an unexpected crash can cause you to lose principal. But looking only at those facts and concluding “investing is dangerous” is shallow thinking.

Savings Is the Same as Investing in the Japanese Yen

If you don’t invest, you save. But saving is simply another way of saying “I’m investing in Japanese yen.”

And yen savings come with risks: inflation erodes their value, and yen depreciation reduces their value relative to other currencies.

To put it simply: if you have ¥1,000,000 saved and something that costs ¥100 today costs ¥200 in a few years, your million yen buys half as much. That is the risk of the yen losing value.

Japan experienced nearly 30 years of deflation, so this rarely felt real. But since 2022, annual inflation of 2% or more has arrived and is here to stay. In that sense, saving in yen means your money loses a few percent of its value every year.

A concrete example: the USD/JPY rate was around 108 yen per dollar in early 2020, but around 145 yen in early 2024. The yen lost enormous value relative to the dollar in just four years.

To maintain or grow the value of your assets in this environment, investing in something beyond cash savings has become a widely accepted necessity.

The Two Greatest Benefits of Investing: Diversification and Compound Interest

The two greatest advantages of investing, in my view, are risk diversification and the compound interest effect.

Risk diversification: If you keep all ¥1,000,000 in yen savings, you bear the full impact of yen depreciation. But if you split it — ¥500,000 in yen and ¥500,000 in dollars — the dollar portion is protected from yen weakness. When you convert the dollars back to yen, you have more than if you’d stayed in yen alone. This is diversification.

While stocks and other risk assets carry the danger of principal loss, they also tend to be inflation-resistant — because inflation means the currency is losing value, and prices (including stock prices) adjust upward accordingly.

Combining stable savings with stock investments lets you weather sudden changes in society while also pursuing growth.

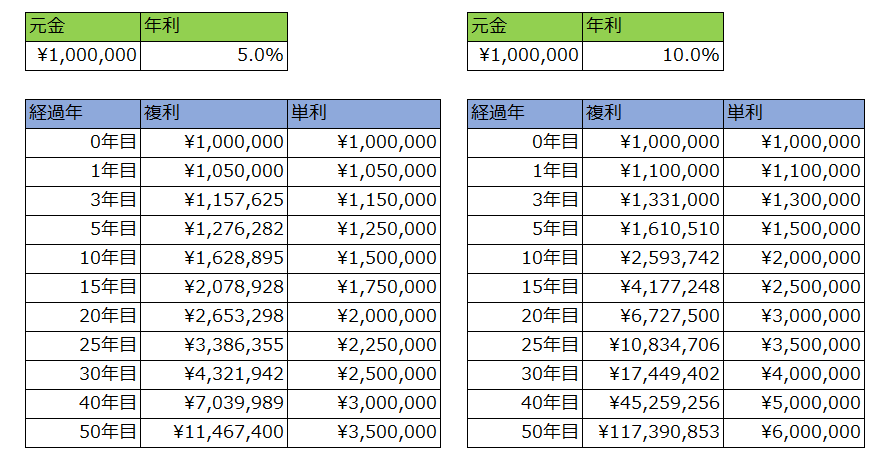

Then there is the compound interest effect — the most powerful force in wealth building. Compound interest means that when your investment earns returns, those returns are added to the principal, and future returns are calculated on the enlarged total. Simple interest, by contrast, only applies returns to the original principal.

The compound effect is strongest when you earn a stable annual return. The table below shows what happens starting with ¥1,000,000 at 5% annual returns (left) and 10% annual returns (right).

By reinvesting returns rather than spending them, compound growth takes over. At 5% annually, you end up with 1.7x more than simple interest after 30 years. At 10% annually, ¥1,000,000 exceeds ¥10,000,000 after 25 years and passes ¥100,000,000 after 50 years.

This is what Albert Einstein — famous for relativity — reportedly called “the greatest invention of mankind.” It is knowledge you absolutely must understand before investing.

Of course, dividends and shareholder perks (for Japanese stocks) add additional income streams worth considering.

How to Reduce Investment Risk

The main reason investment anxiety persists is insufficient knowledge. Building up knowledge is the most effective way to address it.

That said, learning everything at an expert level is too high a bar. Here are the minimum essentials a beginner needs:

- Know the market benchmarks

- Know the investment approaches

- Know the investment products

Also helpful: a basic understanding of current market conditions, available tax-advantaged programs, and relevant regulations.

Know the Market Benchmarks

Knowing benchmarks is essential to avoid being duped by scam products.

Think about grocery shopping — you know the typical price of items. If something suddenly cost 10 times more, you’d hesitate to buy it unless it was absolutely necessary.

Knowing market benchmarks is far more important than it sounds, because it lets you spot anything claiming returns that are wildly out of line with reality.

Investment returns vary widely. Some individuals lose over 50% in a year; a tiny few gain over 1,000%. I’ve personally multiplied crypto assets by over 1,000% — but targeting such returns from day one is not realistic, and sustaining them year after year is impossible.

The clearest benchmark: the average annual return of Warren Buffett, the most successful investor in history, is approximately 20%. That may not sound impressive, but recall what compound interest does: starting with ¥1,000,000 at 20% annually for 50 years yields about ¥9.1 billion.

The implication: any product claiming consistent returns above 20% annually is extremely suspicious or carries extreme risk. If someone could deliver 20%+ reliably, they’d already be wealthier than Buffett.

For context: professional fund managers typically average 3–4% annually, and most individual investors end up with negative average returns.

This is the reality of investing. But by choosing the right approach and the right products, you can minimize risk and maximize returns.

Know the Investment Approaches

The main approaches differ by holding period — how long between buying and selling. Definitions vary slightly, but roughly:

- Short-term trading (multiple trades per day)

- Swing trading (days to weeks)

- Medium-term investing (months to under a year)

- Long-term investing (one year to decades)

The conclusion up front: for beginners who want to preserve and grow assets, long-term investing is the only real choice.

Short-Term Trading (Day Trading)

Day traders buy and sell multiple times within a single day. It requires being glued to the market constantly — impossible for most salaried employees.

The main advantage: you don’t hold positions overnight, so you largely avoid the catastrophic losses that occur when a market crash hits and you’re holding positions.

The main disadvantage: every trade incurs fees, making it easy to end up in the red overall. Predicting whether a price will go up or down in real time is incredibly difficult and luck-dependent.

This is the least suitable approach for beginners among those listed here.

Swing Trading

Swing trading means holding a position for days to weeks, selling when the price rises as anticipated (or short-selling and buying back).

Example: if you expect a certain company to make a major announcement in the next week to a month, you buy the stock in advance, then sell after the news breaks and the price jumps.

This requires research and doesn’t always work — the news may not materialize, or the price may not move as much as expected. It is also susceptible to market crashes.

That said, for those who know an industry well, it can be very effective. Focus on sectors attracting capital — in 2024, AI-related stocks are one example.

Suitable for those who want significant gains and are willing to do research and accept higher risk.

Medium-Term Investing

Medium-term investing is similar to swing trading but with a holding period of months to about a year.

The logic is similar, but with a longer horizon, you can invest in trending sectors and simply wait for a significant news event to emerge — reducing the need for precise timing.

Be aware that sector trends change over multi-year periods, so this approach isn’t suited to very long holding periods.

Good for those who want reasonable returns while keeping risk moderate, without spending a lot of time researching.

Long-Term Investing

Long-term investing means holding positions for one year or more — potentially decades.

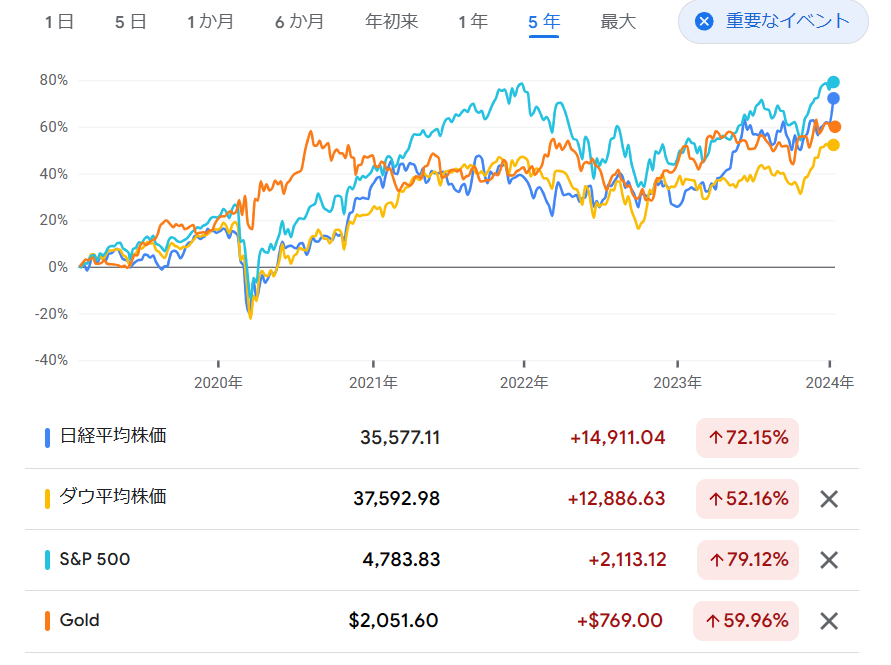

Any sound investment product tends to appreciate in value over the long run. Looking at Japan’s stock market, the U.S. stock market, and gold over five years:

Even over just five years, markets were up 50%+. And even if a major crash occurs, markets have historically recovered and exceeded previous highs over multi-decade timeframes.

That said, Japan’s bubble-era peak wasn’t surpassed for over 30 years — and individual stocks can sometimes never recover, or companies can go bankrupt. Product selection at the start is critical for long-term investing.

Choose correctly, however, and you can simply hold and watch your wealth grow over the years without paying it much attention. This is why ACWI and similar products are so widely recommended by influencers and bloggers.

Long-term investing is the easiest and most reliable approach for beginners, minimizing risk while delivering stable annual returns through compounding.

Even Warren Buffett — the world’s greatest investor — uses long-term investing as his primary strategy. That tells you all you need to know about its credentials.

Know the Investment Products

Stocks

Stocks are the king of investments. Japanese stocks are the most accessible starting point, though foreign stocks (especially U.S. stocks) are increasingly popular.

Owning shares gives you a stake in the company itself — not just a financial instrument. In practice, shares are mostly bought and sold as investments, but they can also be used to acquire controlling interests.

To buy stocks in Japan, you open an account with a brokerage and purchase shares listed on the stock exchange.

As of April 2022, Japan’s market tiers were renamed from “TSE First Section” etc. to “Prime,” “Standard,” and “Growth.” The old names are still commonly heard but are no longer in use.

Roughly: major corporations like Toyota belong to “Prime”; mid-tier companies to “Standard”; early-stage growth companies to “Growth.”

Key advantages of stocks:

- Easy to start (open an account, deposit, buy)

- Enormous selection (~3,900 listed companies in Japan)

- Regulated and relatively trustworthy

- Potential for major gains (some stocks gain 10x in a year)

- Dividends and shareholder perks beyond price appreciation

- Can start with small amounts (mini-lot trading available)

- Real-time trading

- Low fees and ~20% tax (tax-free in a NISA account)

- No tax filing required if using a specific account

Main disadvantage: risk of principal loss (a falling stock can easily lose half its value).

Stocks have a long history and many investor-friendly features — they are the natural starting point. But the breadth of choices and the need to research individual companies creates a learning curve.

If you’re not confident about doing your own research, investment trusts or ETFs (covered below) are a better starting point.

FX (Forex)

FX (Foreign Exchange) involves profiting from the difference between currency pairs, such as USD/JPY. As mentioned above, the dollar went from about 108 yen to 145 yen in four years — a significant move.

Holding dollars as a hedge against yen weakness is a valid strategy, but U.S.-dollar-denominated stock investments would typically outperform simply holding dollars.

More importantly, short-term leveraged FX trading is essentially gambling, not investing. It is not recommended for anyone focused on preserving and growing wealth.

Cryptocurrency (Bitcoin, etc.)

Cryptocurrency was called “virtual currency” in Japan until the Financial Services Agency officially renamed it “crypto assets” (暗号資産) in May 2020, coinciding with major regulatory updates to the Payment Services Act and Financial Instruments and Exchange Act.

Crypto is now legally recognized as an investment asset, and U.S. approval of Bitcoin ETFs has further boosted its profile.

Key characteristics:

- Easy to start (open an exchange account and deposit)

- Extremely high risk and high return (far more volatile than stocks)

- Enormous selection (over 20,000 cryptocurrencies exist)

- Real-time trading

- Low reliability (Bitcoin and major coins are more trustworthy; small coins are extremely risky)

- High fees and taxes (crypto income is classified as “miscellaneous income” in Japan, taxed up to ~55%)

- Unclear how it will adapt to future technological changes

- Annual tax filing required

The chart above compares Bitcoin, the Nikkei Average, and the Dow over five years. Bitcoin gained 1,413% — dwarfing the ~50–70% gains for the traditional indices. But the swings are enormous too.

Many people choose crypto over stocks for this reason, especially those with limited capital looking for a big breakthrough.

I’ve personally multiplied crypto holdings significantly when capital was limited, so I understand the appeal. But the 55% tax rate in Japan means a large portion of gains disappears before you see them — and many crypto investors end up with disappointingly little after tax.

Crypto is best suited to those with limited capital who are willing to accept extreme risk in pursuit of rapid, large gains — not those focused on steady wealth preservation and growth. I generally don’t recommend it to investment beginners.

Investment Trusts and ETFs (ACWI and S&P500 in focus)

An investment trust (fund) pools money from many investors, which a professional manager then invests in stocks, bonds, and other assets on their behalf.

If the manager achieves 10% annual returns, your investment grows by 10%. If they lose 10%, your investment shrinks by 10%.

Unlike individual stocks — where you invest in one company — investment trusts invest in many companies and assets simultaneously, delivering maximum risk diversification benefit.

An ETF (Exchange-Traded Fund) is a type of investment trust that trades on stock exchanges like the Tokyo Stock Exchange.

Investment trusts are relatively low-risk because of professional management and diversification, making them an ideal starting point for beginners who don’t know which individual stocks to pick.

One major downside: management fees (trust fees) can be high. Even if the portfolio gains 10%, you might pay 0.5–2% in annual fees, leaving your net gain lower. Then ~20% tax is applied on top.

In recent years, the ACWI and S&P500 have become extremely popular — to the point where many say “if you’re starting out, just pick one of these two.”

ACWI (All-Country World Equity Index Fund)

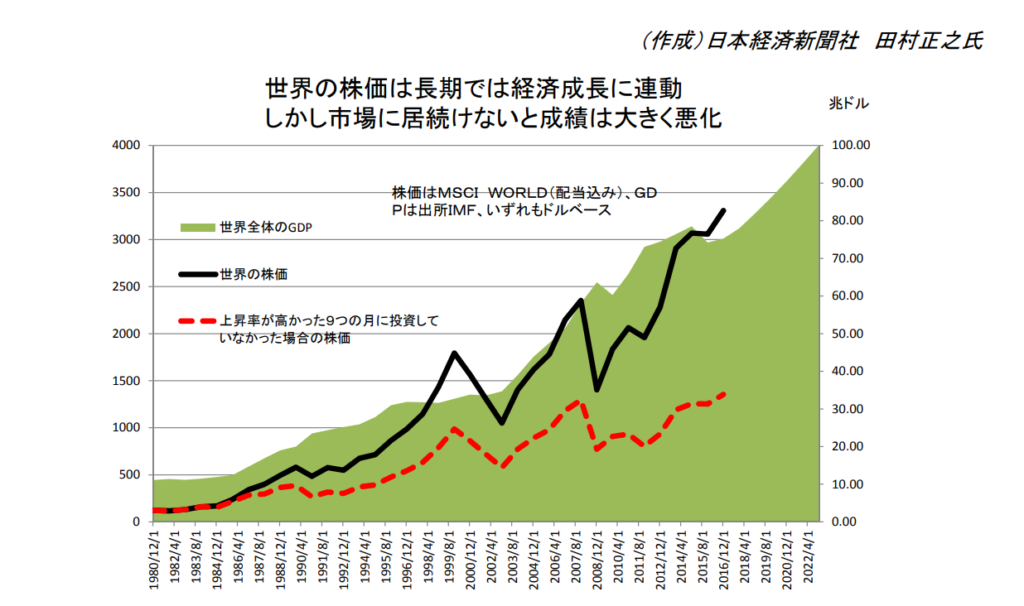

The ACWI (“Orukan” in Japan) invests across all global stock markets in proportion to each country’s market index — maximizing both risk diversification and compound interest benefits.

The global stock market has grown consistently over time, even recovering from major crises. As long as that trend continues, the ACWI grows with it.

Expected annual average return based on the past 30 years: approximately 6–9%. Accounting for inflation, this level of compound growth represents very solid, stable asset management.

The ACWI’s trust fees are also among the lowest available, thanks to intense competition — minimizing the main downside of investment trusts.

S&P500

The S&P500 tracks 500 major U.S. companies and is one of the most widely followed U.S. indices alongside the Dow Jones.

An S&P500 investment trust tracks this index — investing proportionally in all 500 companies. If the index rises, your investment grows; if it falls, it shrinks.

Compared to the ACWI, the S&P500 concentrates entirely on the U.S. — making it more vulnerable to a U.S.-specific crash. That said, since the U.S. makes up the largest share of the global stock market, a U.S. crash would almost certainly pull the ACWI down as well.

The S&P500 has historically outperformed the ACWI, reflecting the dominance of the U.S. economy over recent decades. This is why many investors who want slightly higher returns choose the S&P500 over the ACWI.

Both are among the most beginner-friendly investment products available — many people buy both to further diversify.

Real Estate

Real estate investing involves buying and selling actual land and buildings, and it predates the stock market in terms of history.

To be honest: beginners should not touch real estate investing. It requires knowledge of relevant laws, understanding of specific properties’ characteristics, and ongoing management of a physical asset — the learning curve is extremely steep.

The real estate industry also has a notoriously murky side, with far more scam-like products than in stocks or investment trusts. Spotting them requires expertise.

Various beginner-friendly real estate services have emerged, but for similar expected returns, stocks and investment trusts are far simpler.

With sufficient expertise, real estate can be extremely effective — some landlords live entirely off passive rental income. But for now, beginners should avoid it and revisit the idea after building up deeper investment knowledge.

Government Bonds

Government bonds are debt instruments issued by the government — you lend money for a set period, receive interest, and get your principal back at maturity. They are one of the few principal-guaranteed investment products.

The trade-off is very low returns: typically 0.05–0.6% annually, rarely exceeding 1%. After accounting for ~2% annual inflation, you are effectively losing purchasing power.

Large institutional investors use government bonds as stable, low-yield components of a diversified portfolio. For individuals, the returns are too low to recommend — unless yields rise meaningfully in the future.

Gold and Platinum

Unlike stocks and investment trusts, which tend to fall during financial crises, gold and platinum tend to rise during such events — making them valuable for diversification.

Gold in particular has been a symbol of wealth throughout history, with a relatively stable long-term upward trend. However, as the chart below shows, returns over the past decade have been modest.

No dividends or coupons are paid, so gold and platinum are primarily useful as wealth preservation tools rather than growth vehicles — and for those who want to hold tangible physical assets.

Other Investment Products

Products offered by specific companies or organizations beyond those listed above generally should not be used as investment targets — especially by beginners.

Compared to the products above, such offerings often have poor social credibility, minimal legal regulation, and inadequate investor protection in the event of disputes.

They frequently claim higher returns or principal guarantees, but in reality they carry extreme risk or are outright scams. Don’t trust your hard-earned assets to them.

What Is NISA?

Finally, a brief overview of the much-discussed NISA.

Simply put, NISA is a system where you open a dedicated NISA account and, trades made through that account are exempt from the approximately 20% tax normally applied to gains — up to a certain annual limit.

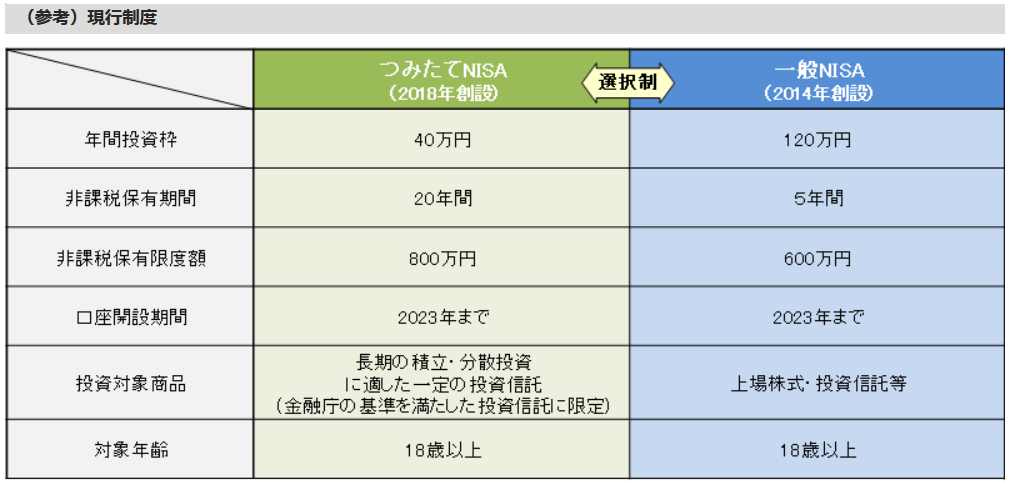

Old NISA came in three types: the “General NISA” (up to ¥1.2 million/year, tax-free for 5 years), the “Tsumitate NISA” (up to ¥400,000/year, tax-free for 20 years), and the “Junior NISA” for minors.

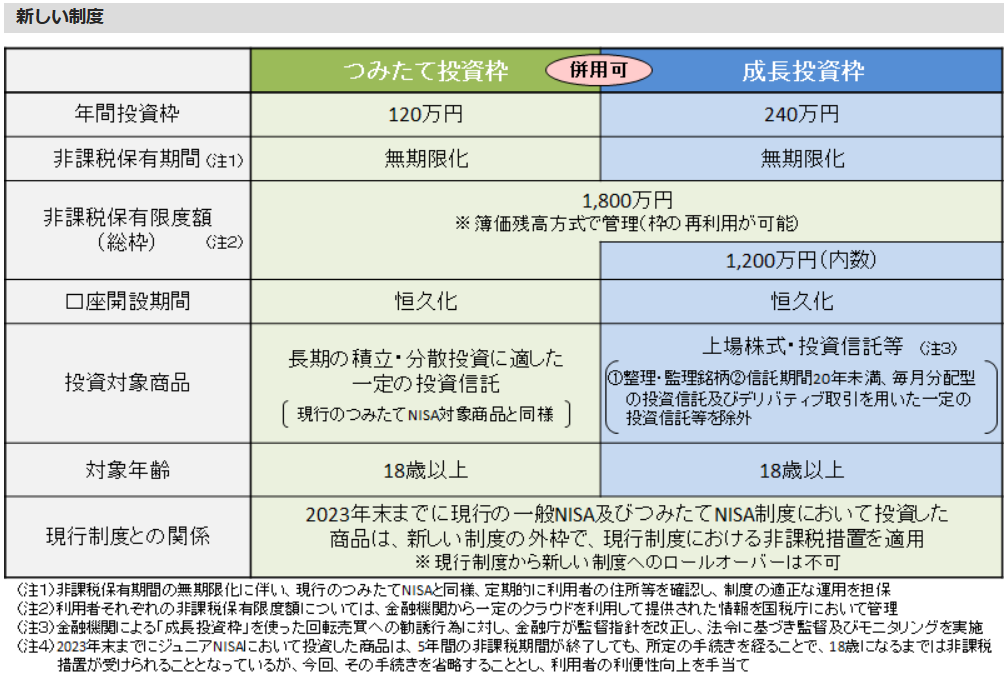

New NISA, launched January 1, 2024, renamed the General NISA to “Growth Investment Allowance” (raised to ¥2.4 million/year, unlimited tax-free period) and the Tsumitate NISA to “Accumulation Investment Allowance” (raised to ¥1.2 million/year, unlimited tax-free period). The Junior NISA was discontinued.

New NISA allows up to ¥3.6 million per year combined to be managed completely tax-free, replacing the usual ~20% tax. The only real inconvenience is the application paperwork — the system is overwhelmingly advantageous for anyone who uses it.

For comparison charts of New NISA vs. Old NISA, see the Financial Services Agency’s official page.

Summary

This turned out longer than I intended, but if you’ve read this far, you have a solid foundation in investment basics.

Of course, this article only scratches the surface. To go deeper on any particular topic, additional study on your own will be needed.

My personal take on how to allocate assets for the best balance:

Savings (20%) + ACWI / S&P500 (60%) + Individual Stocks (20%)

Keep about 20% in liquid cash savings — unexpected cash needs will always arise. Adjust based on your own financial situation.

Putting about half your remaining assets into the ACWI or S&P500 provides stable preservation and growth. Individual stocks can be skipped at first, but as your knowledge grows, finding companies you truly believe in and investing in them adds a rewarding dimension to investing.

Growing your knowledge is just as important as growing your assets. Buying the ACWI mindlessly without any financial education leaves you potentially unable to adapt when the world changes — so I personally don’t love the idea of putting everything in a single fund and forgetting about it.

That concludes my overview.

I may write more detailed articles on individual topics in the future — check back if you’re interested. I’ve also written articles on value investing indicators and more, linked below.

Also popular with readers