Introduction

Since the New NISA (Japan’s revised tax-free investment program) system launched on January 1, 2024, people who had never invested before have been entering the investment world in growing numbers.

In this article, I want to explore how the investment landscape is expected to change now that New NISA is up and running.

What Is NISA, Anyway?

Before diving into predictions, let me briefly explain what NISA is, since some readers may be asking that very question.

The NISA system itself had been in place for about 10 years before the New NISA launched in January 2024. I’ll refer to the previous version as “Old NISA” here.

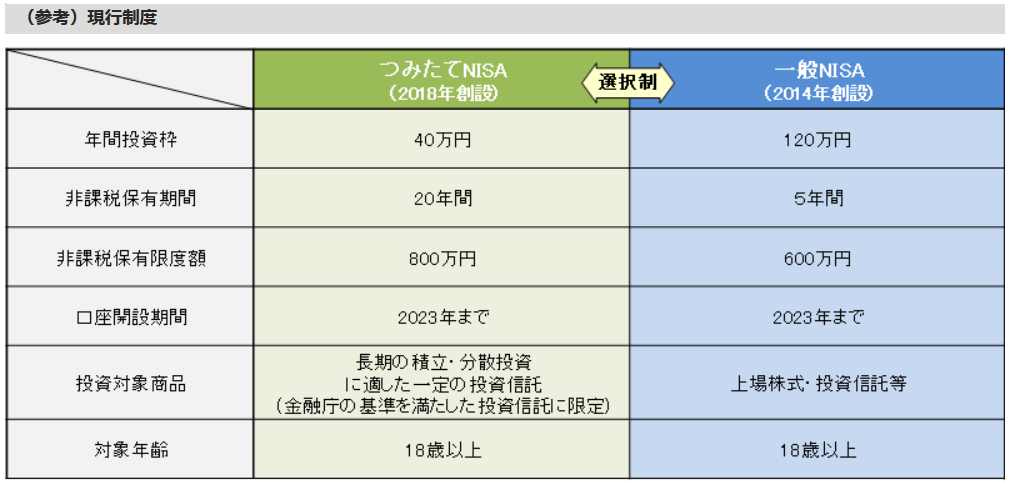

Simply put, Old NISA was a system where you open a dedicated NISA account, and trades made through that account are exempt from the roughly 20% tax normally applied to investment gains — up to a certain annual limit.

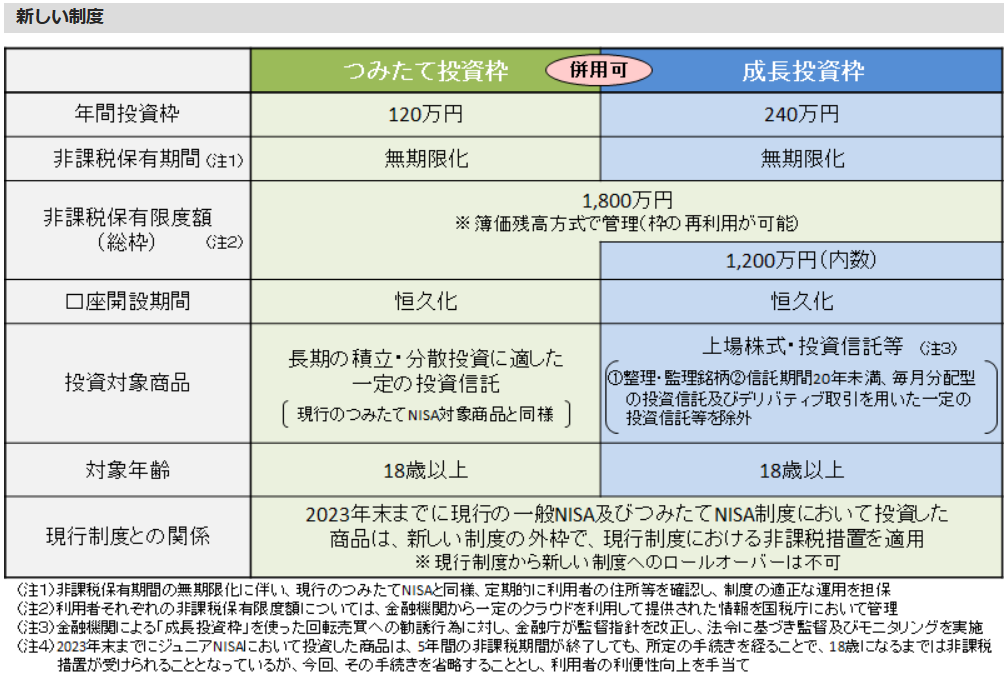

Old NISA came in three flavors: the “General NISA” (up to ¥1.2 million per year, tax-exempt for up to 5 years), the “Tsumitate (Accumulation) NISA” (up to ¥400,000 per year, tax-exempt for up to 20 years), and the “Junior NISA” for minors.

New NISA keeps the same core concept but brings major improvements. The “General NISA” was renamed the “Growth Investment Allowance,” with the annual limit raised to ¥2.4 million and the tax-exempt period extended from 5 years to unlimited. The “Tsumitate NISA” became the “Accumulation Investment Allowance,” with the annual limit raised to ¥1.2 million and the period extended from 20 years to unlimited. Unfortunately, the Junior NISA was abolished (perhaps because uptake was low).

These major changes took effect on January 1, 2024, and the new system is what is called “New NISA.”

In short: New NISA allows you to invest up to ¥3.6 million per year combined across the Growth and Accumulation allowances, completely tax-free instead of paying the usual ~20% tax.

Compared to the ¥1.6 million combined annual limit under Old NISA, New NISA more than doubles the tax-free allowance — and makes it unlimited in duration. This is an extraordinary improvement.

There are essentially no downsides to using this system; the only inconvenience is the paperwork to open an account. It is overwhelmingly advantageous to use it.

The government’s intention is clear: by creating such a generous incentive, it hopes to channel citizens’ money into the markets and stimulate the economy.

The Financial Services Agency’s official page includes a comparison table of New NISA vs. Old NISA — check it out for reference.

What Will Change Under New NISA?

Now for the main topic: what changes can we expect as a result of the New NISA system? Both popular commentary and my own thinking point to the following:

- Expansion of the domestic stock market

- Growing interest in international investing

- Increase in individual investors (especially younger generations)

- Long-term investing becoming mainstream

- Rising importance of financial education (financial literacy)

- Greater demand for investment-related apps and advisors

Let me explain why each of these is expected.

Domestic Stock Market Expansion

The most direct impact — and the government’s primary goal — will likely be on the domestic stock market.

New NISA’s tax benefits apply to listed stocks, investment trusts, and ETFs (exchange-traded funds). All of these should benefit the domestic stock market in some way.

When people invest directly in stocks, many will naturally gravitate toward domestic stocks they know rather than unfamiliar foreign ones. Investment trusts and ETFs also tend to include a significant share of domestic stocks.

The most popular New NISA product so far is the “ACWI (All-Country World Equity Index Fund).” At first glance it may seem to have little impact on Japan’s market, but Japan is included in the index, so it does provide some support.

Beyond that, New NISA is expected to draw in people who previously had no interest in investing, leading to sustained capital inflows into the domestic stock market over the medium to long term.

One concern is that the domestic market may already be at elevated levels — and it is highly susceptible to overseas shocks, meaning a financial crisis abroad could trigger a rapid contraction. Still, over the medium to long term, the number of market participants and the volume of inflows will almost certainly increase, making domestic stock market expansion highly likely.

Growing Interest in International Investing

New NISA is expected to significantly increase interest in international investing.

The reason is that a considerable share of investors are skeptical about Japanese stocks’ future prospects. Japan has suffered through what is often called “three lost decades” of economic stagnation, and many people are pessimistic about the country’s trajectory.

Such investors tend to show strong interest in foreign stocks or in investment trusts and ETFs that provide diversified exposure to overseas markets.

The fact that the ACWI is the most popular New NISA choice reflects this reality.

Initially, newcomers will likely follow the recommendations of influencers, but over time I expect interest to shift toward other high-yielding international products as well. Even so, the stable ACWI will likely remain the top choice, while interest in higher-risk, higher-return international investments will gradually grow year by year.

Increase in Individual Investors (Especially Younger Generations)

Overlapping somewhat with market expansion, the number of individual investors will certainly increase post-New NISA.

This is partly due to the system’s incentives, but younger generations in particular feel a strong sense of urgency about pension uncertainty and Japan’s economic outlook, driving them to invest for self-protection.

For young people, New NISA is a godsend, and once the barrier to entry is lowered by a first investment, more and more participants will follow.

That said, because Japan’s younger generations are squeezed by low wages and high taxes and social insurance premiums, they have limited savings to begin with — so their market impact will likely take considerable time to materialize.

Long-Term Investing Becoming Mainstream

Japanese individual investors have historically favored short time horizons — many have tried to make money through day trading or swing trading rather than patient, long-term investing.

Traditionally, building wealth through stocks over years at a time is the standard approach, but for cultural reasons or because of Japan’s economic instability, long-term investing never really took root.

With New NISA and the shift toward products like the ACWI, however, more people will start using investing as a vehicle for long-term wealth building rather than a quick money-making scheme. This trend toward longer-term investors is a genuine positive for the economy.

Rising Importance of Financial Education

As interest in investing grows, investment fraud will inevitably rise alongside it. Post-New NISA, financial education (financial literacy) becomes critically important.

Unfortunately, in Japan, openly discussing money and investing is still socially taboo — a very bad habit, in my view. In the United States, financial education is taught in schools, and talking about investing is perfectly normal.

Japan did begin incorporating financial education into high school home economics classes in 2022, but the timing is too late and the content too thin for it to keep pace with emerging problems.

The conclusion: do not rely on the government for financial education. At the individual and household level, we need to equip ourselves with at least the minimum literacy required to avoid investment scams. Above all, be extremely wary of buying investment products recommended by specific influencers.

Greater Demand for Investment Apps and Advisors

As previously non-investing people enter the market, demand for new apps and advisory services to help them will expand.

Many investment-related apps already exist, but new ones will keep appearing. Demand for investment-related YouTube channels and other social media content will also increase.

This will benefit companies developing new apps, as well as operators of finance channels and blogs. And as more educational resources become available, it will be easier to find and debunk misleading or fraudulent information online — a positive development overall.

Summary

This article covered the changes and impacts expected from the New NISA system. New NISA is essentially a system with no downsides, so everyone should at least open an account.

What to buy is a personal decision, but if you want a near-brainless choice, buying the ACWI is the safest bet (low probability of losing money).

More investors in the market can also help stimulate economic activity, making New NISA a system with something for everyone.

For guidance on how to open a NISA account, please refer to the article below.

Also popular with readers